DAILY MARKET OVERVIEW-11.03.2024

- 2024-03-11

- Gold closed the third consecutive week in positive territory.

- XAU/USD technical outlook points to extremely overbought conditions.

- February inflation data will be featured in the US economic calendar next week.

Gold (XAU/USD) gathered bullish momentum and reached a new record high above $2,180 this week, boosted by falling US Treasury bond yields and the broad-based selling pressure surrounding the US Dollar (USD). The pair stays technically overbought ahead of next week’s key inflation data from the US.

Gold price posted largest one-week gain since October

After ending the previous week on a bullish note by surging nearly 2% on Friday, Gold started the new week on a firm footing. After XAU/USD climbed above $2,100, technical buyers showed interest and helped the pair push higher.

The data from the US showed on Tuesday that the ISM Services PMI edged lower to 52.6 in February from 53.4 in January. The Prices Paid Index, the inflation component of the PMI survey, dropped to 58.6 from 64, while the Employment Index slumped to 48 and highlighted a decline in service sector payrolls. The benchmark 10-year US Treasury bond yield broke below 4.2% and the USD came under selling pressure after this data, allowing Gold to preserve its bullish momentum.

Federal Reserve (Fed) Chairman Jerome Powell presented the semi-annual Monetary Policy Report and testified before the House Financial Services Committee on Wednesday. Powell repeated that incoming data will determine when they will start reducing the policy rate and explained that they would like to have greater confidence inflation will move sustainably toward 2% before taking a policy action. When asked about the economic outlook, Powell said that there was no reason to think the economy was “in or facing a significant near-term risk of recession.” Although Powell refrained from providing a fresh clue regarding the timing of the policy pivot, he didn’t shut the door to a rate cut in June. In turn, risk flows dominated the financial markets mid-week, triggering another leg of broad USD weakness, which led to an extended uptrend in Gold.

Friday, the 10-year US yield dropped to its weakest level in a month below 4.1% after the US Bureau of Labor Statistics (BLS) revised the fourth-quarter Unit Labor Costs lower to 0.4% from 0.5% in the initial estimate. Additionally, the US Department of Labor reported that there were 217,000 Initial Jobless Claims in the week ending March 12, matching the previous week’s print. Gold closed the seventh consecutive trading day in positive territory on Thursday and reached a new all-time high above $2,160. Finally recording an all time high as my predictions of $2.195.

Nonfarm Payrolls in the US rose by 275,000 in February, the BLS reported on Friday. This reading surpassed the market expectation of 200,000. On a negative note, January’s increase of 353,000 was revised lower to 229,000. Other details of the jobs report showed that the Unemployment Rate rose to 3.9% from 3.7%, while the Labor Force Participation Rate held steady at 62.5%. The USD came under renewed selling pressure with the initial reaction and Gold advanced beyond $2,180.

Gold price could have a short-lasting reaction to inflation data

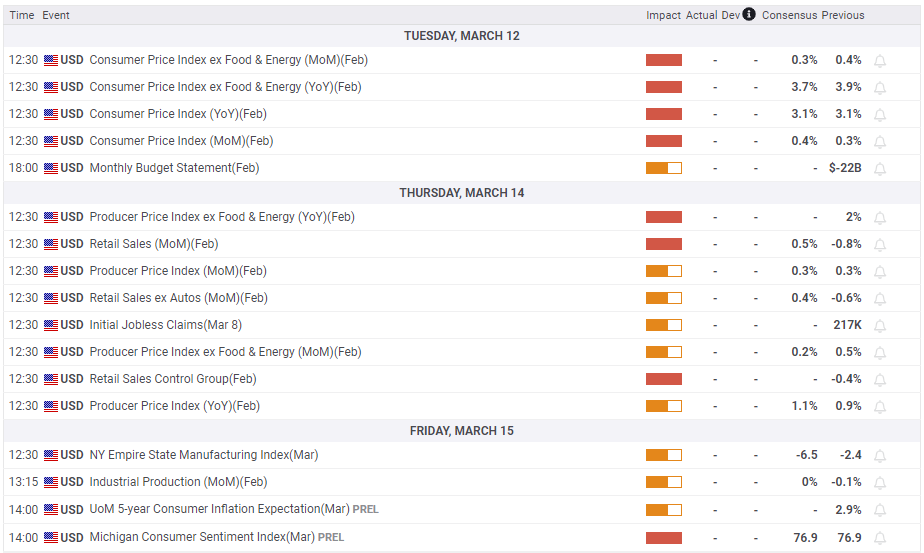

The BLS will release Consumer Price Index data for February on Tuesday. On a monthly basis, the CPI and the Core CPI, which excludes volatile food and energy prices, are forecast to rise 0.4% and 0.3%, respectively.

The CME FedWatch Tool shows that markets are pricing in a nearly 80% probability that the Fed will lower the policy rate in June, while the odds of a 25 basis points rate reduction in May holds around 25%.

Ahead of the June meeting, investors will have three more CPI releases, excluding February, to assess. Hence, the February CPI reading is unlikely to alter the market positioning in a significant way. Only a monthly Core CPI print close to 0% could revive expectations for a rate cut in May and further weigh on the USD. Although a strong Core CPI increase in February is unlikely to make market participants lean toward a no-change in the Fed interest rate in June, the initial reaction could trigger a downward correction in XAU/USD, given the USD’s oversold nature.

The US economic docket will feature February Retail Sales on Thursday and the Fed will publish February Industrial Production data on Friday.

In the meantime, the Fed will be in the blackout period ahead of the March 19-20monetary policy meeting. Following Tuesday’s inflation data, investors could shift focus to technical developments in XAU/USD for trading opportunities.

GBPUSD ANALYSIS

- UK labour market in the spotlight as wage pressures remain elevated

- GDP data to also be watched as UK in technical recession

- Pound starts March on firmer footing, will the data support further gains?

- Employment report is due Tuesday and GDP figures on Wednesday at 07:00 GMT

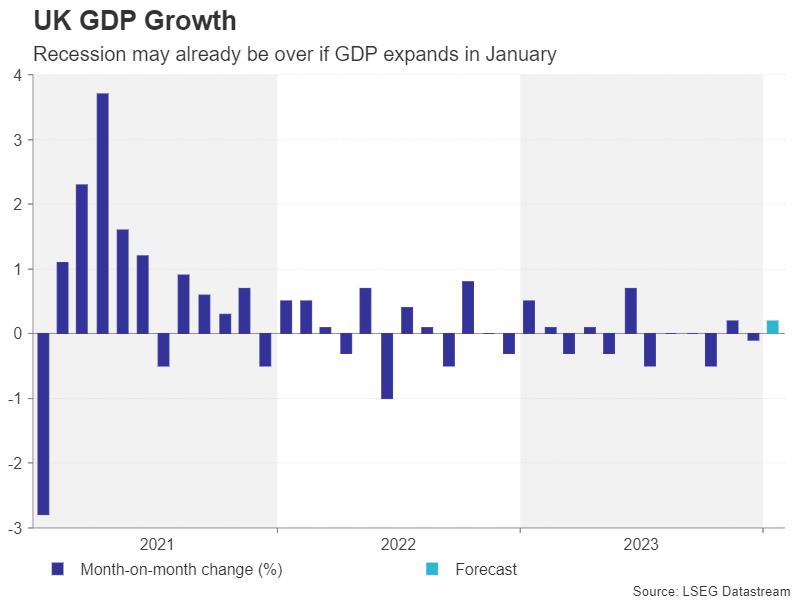

Stagnation vs recession

The British economy along with Japan became the first of the major economies in the post-pandemic era to slip into a technical recession in the second half of 2023. Germany narrowly avoided one, while the United States grew at the fastest pace in two years. GDP figures are prone to significant revisions, particularly UK ones, so it’s probably not a good idea to overdo the comparisons.

However, what is clear is that growth in Europe and the UK has stagnated and politicians don’t seem to have a very strong strategy of rectifying that. Such an economic backdrop would normally be bad news for the euro and pound against the mighty US dollar, but the inflation landscape is much more identical on both sides of the Atlantic, hence, there is much less of a divergence when it comes to monetary policy.

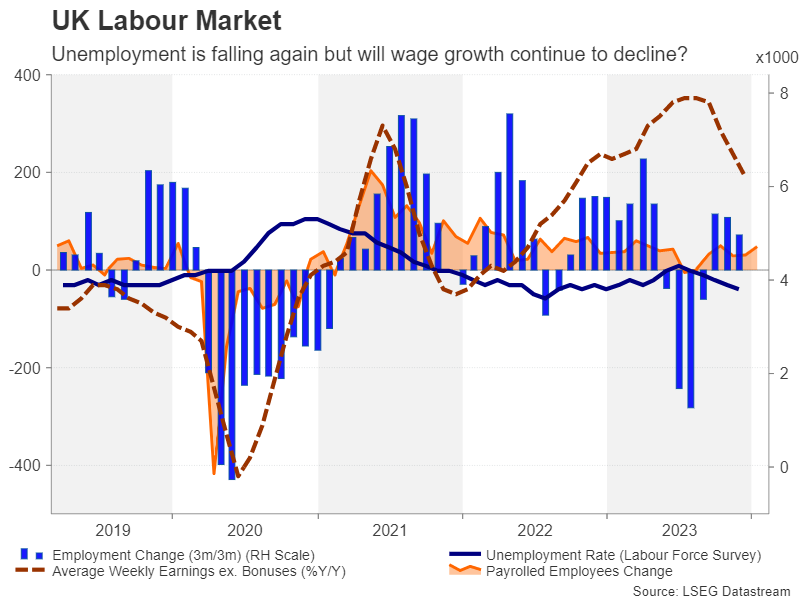

UK labour market may be heating up again

This also solidifies inflation as the primary data driver for sterling. Nevertheless, next week’s employment numbers and GDP readings will be important in setting the mood ahead of the CPI report on March 20 and the Bank of England meeting a day later. Britain’s labour market has bounced back in recent months, with the jobless rate falling to 3.8% in the three months to December.

Further employment growth in the three months to January would suggest that an economic recovery is already underway. However, with the Office for National Statistics admitting that its employment surveys have become less reliable lately and that a fix is months away, wage growth will likely be the main focus for both investors and policymakers.

High wage growth still a problem

Average weekly earnings excluding bonuses stood at 6.2% y/y in the three months to December, having eased substantially from the high of 7.9% over the summer. A further cooldown in wage growth in January would allay concerns about persisting wage pressures.

On Wednesday, GDP data is expected to show that the UK economy grew modestly by about 0.2% in January after contracting by 0.1% m/m in December. Industrial production numbers are also due the same day.

Dollar bulls hoping for hot CPI data

Other indicators on next week’s schedule include the Empire State manufacturing index, industrial production and the University of Michigan’s preliminary estimate of consumer sentiment in March, all due on Friday.

For the US dollar, the main risk is upside surprises in the CPI prints, which have the potential to cast doubt on a June rate hike that investors have pinned their hopes on. A hot CPI report would be damaging for risk assets but positive for the greenback, which badly needs a lift after being on the backfoot since mid-February. Aside from the data, a slew of bond auctions by the Treasury Department could also inject some volatility into bond, FX and equity markets.

Will UK GDP point to a rebound?

The pound will be in the limelight too over the coming week as labour market stats and the monthly GDP reading are on the UK agenda. Employment in the UK slumped last summer as the economy shrunk, but has been rising since October, with the jobless rate falling again to 3.8%. If Tuesday’s report points to a further improvement in the labour market in January, it would ease concerns about a sharp recession.

Prepared by: Mr. SAM KIMA, Senior Vice President